Solar Market Insight Report Q4 2025

In Q3 2025, the residential segment installed 1,088 MWdc of solar capacity, declining 4% year-over-year and quarter-over-quarter. Despite an industry rush to bring projects online this year to

In Q3 2025, the residential segment installed 1,088 MWdc of solar capacity, declining 4% year-over-year and quarter-over-quarter. Despite an industry rush to bring projects online ...

HOME / Analysis of the current status of domestic solar inverters - LUP MICROGRID

Analysis of the current status of domestic solar inverters - LUP MICROGRID [PDF]

In Q3 2025, the residential segment installed 1,088 MWdc of solar capacity, declining 4% year-over-year and quarter-over-quarter. Despite an industry rush to bring projects online this year to

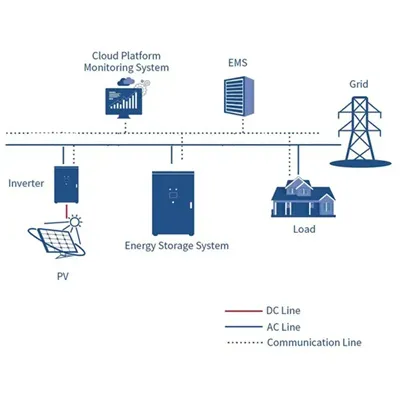

Based on the conversion technology employed, solar inverters are categorized into three types: grid-connected, standalone, and hybrid. Grid-connected solar inverters dominate, accounting for nearly

The residential solar PV inverter market size exceeded USD 4.2 billion in 2024 and is expected to grow at a CAGR of 5.8% from 2025 to 2034, driven by falling

With global solar installations expected to reach 2.3 terawatts by 2025, inverters play a pivotal role in enabling grid stability and energy efficiency. This article breaks down key drivers, challenges, and

The solar inverter market report provides an extensive analysis of market segmentation, technological evolution, regional performance, competitive landscape, and investment trends.

The residential solar PV inverter market is expanding steadily due to rising adoption of renewable energy solutions, declining solar module costs, and supportive government incentives for

Although these conditions might appear bleak—a delay on the path to net zero and yet another setback in an industry that has taken decades to take

As the energy crisis fueled by Russia''s invasion of Ukraine has subsided, demand for residential solar systems in the EU has declined and several residential solar incentive schemes

The quantitative analysis demonstrates that conventional inverter topologies have reached fundamental performance limits, with efficiency improvements following diminishing returns where

This report explores the current state of these supply chain challenges, with a specific focus on the impact of the BABA requirements and the associated complexities in inverter manufacturing and supply.